Raising in China

Promoting: HICOOL Global Entrepreneur Summit and Entrepreneurship Competition. Read more here.

Raising in the UK

Venture List

London continued to draw the vast majority of British VC investment, attracting £16.4bn compared to £6.2bn across the rest of the country combined. There were 1,443 VC deals across the UK’s regions in 2022 compared to London’s 1,770 deals.

UK-based start-ups raised $18 billion VC funding during January to July 2022, finds GlobalData

Apart from being the top European market, the UK is also among the top five markets for global venture capital (VC) funding activity, found GlobalData. According to the leading data and analytics company, a total of 1,083 VC funding deals were announced in the UK during January-July 2022 while the disclosed funding value of these deals stood at $18 billion.

An analysis of GlobalData’s Financial Deals Database reveals that VC funding activity in 2022 so far has showcased a fluctuating trend in the UK with July reversing the growth trend witnessed during the previous month. The UK witnessed a 32.7% decrease in VC funding deal volume in July compared to the previous month while the corresponding deal value shrunk by 43.6%.

Aurojyoti Bose, Lead Analyst at GlobalData, comments: “The subdued VC funding activity is indicative of prevailing market volatility and investor concerns with rising inflation, recession fears and geopolitical tensions denting deal-making sentiments.”

Nevertheless, investors did showcase their confidence in some UK start-ups by placing big bets despite unfavorable market conditions. Some of these notable VC funding deals announced during January to July 2022 in the UK included the $1 billion raised by Checkout, $621.7 million raised by SumUp, $377 million raised by Bloom Financial Group, $300 million raised by Oxford Science Enterprises, $220 million funding raised by Multiverse, $200 million funding raised by Paddle.com, and around $190 million raised by PrimaryBid.

Note: Historic data may change as some deals may be added to previous months because of a delay in disclosing information to the public domain

Recent VC trends of UK, Ireland in five charts

Venture capital deal activity in the UK and Ireland has remained robust in the first half of 2022 as both countries weather a cost-of-living crisis and the prospect of a long recession.

While investors continued to pour capital into the region, current market conditions are expected to flatten dealmaking activity toward the end of the year.

Here’s a look at five VC charts from PitchBook’s UK & Ireland Private Capital Breakdown, illustrating key trends across deals, exits and fundraising.

Capital raised by VC-backed companies in the UK and Ireland matched the pace set last year with £15.4 billion (around $15.3 billion) invested in H1—just over half of 2021’s £28.2 billion total. The region has seen a slowdown in deal volume with the number of rounds falling short of 2021’s halfway mark—1,879 in H1 2022 compared with 3,857 for the whole of last year.

This deceleration in deal count is expected to continue, as the effects of rising inflation, which hit a 40-year high in July, and the worsening condition of the overall economy become clearer for the asset class.

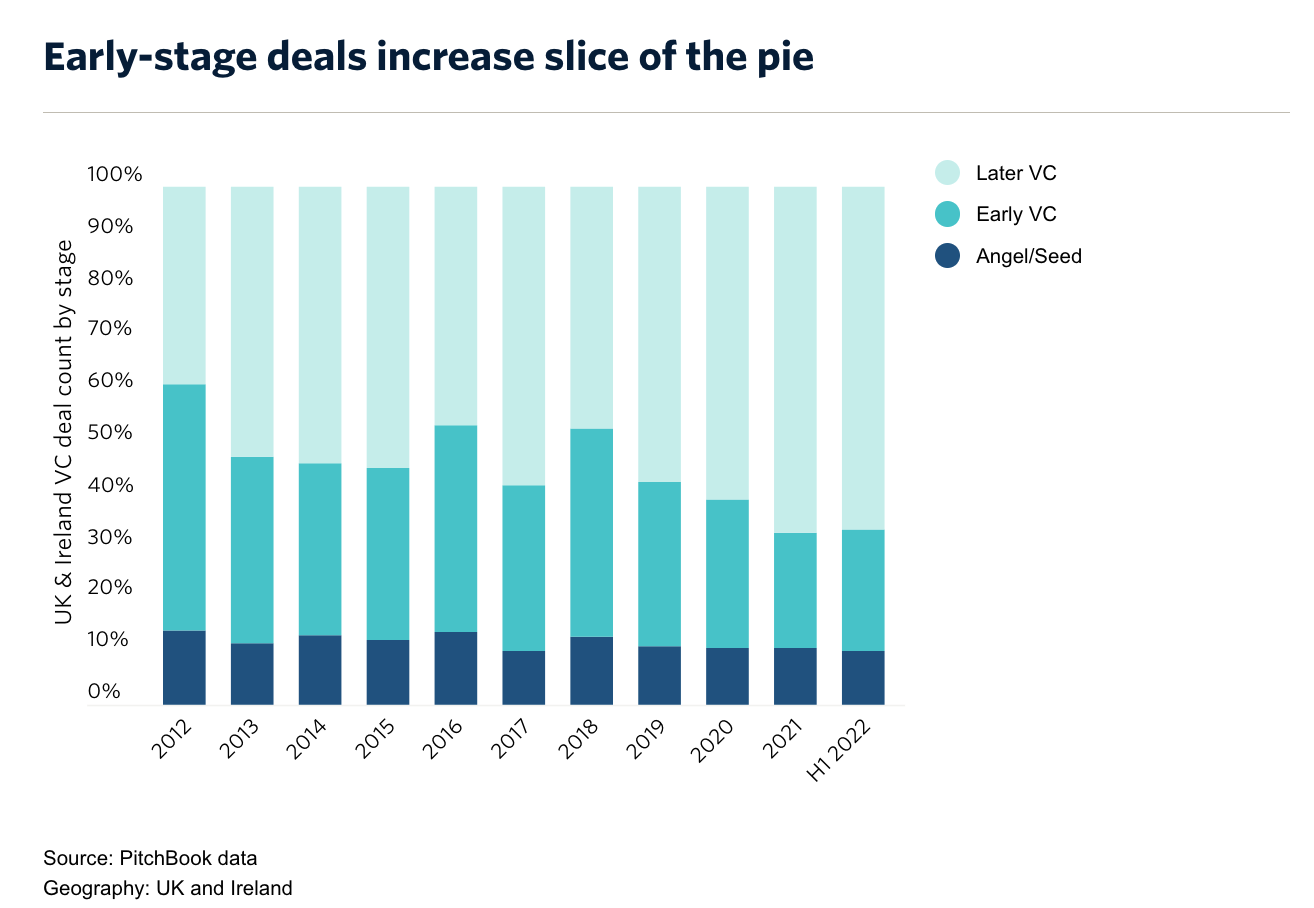

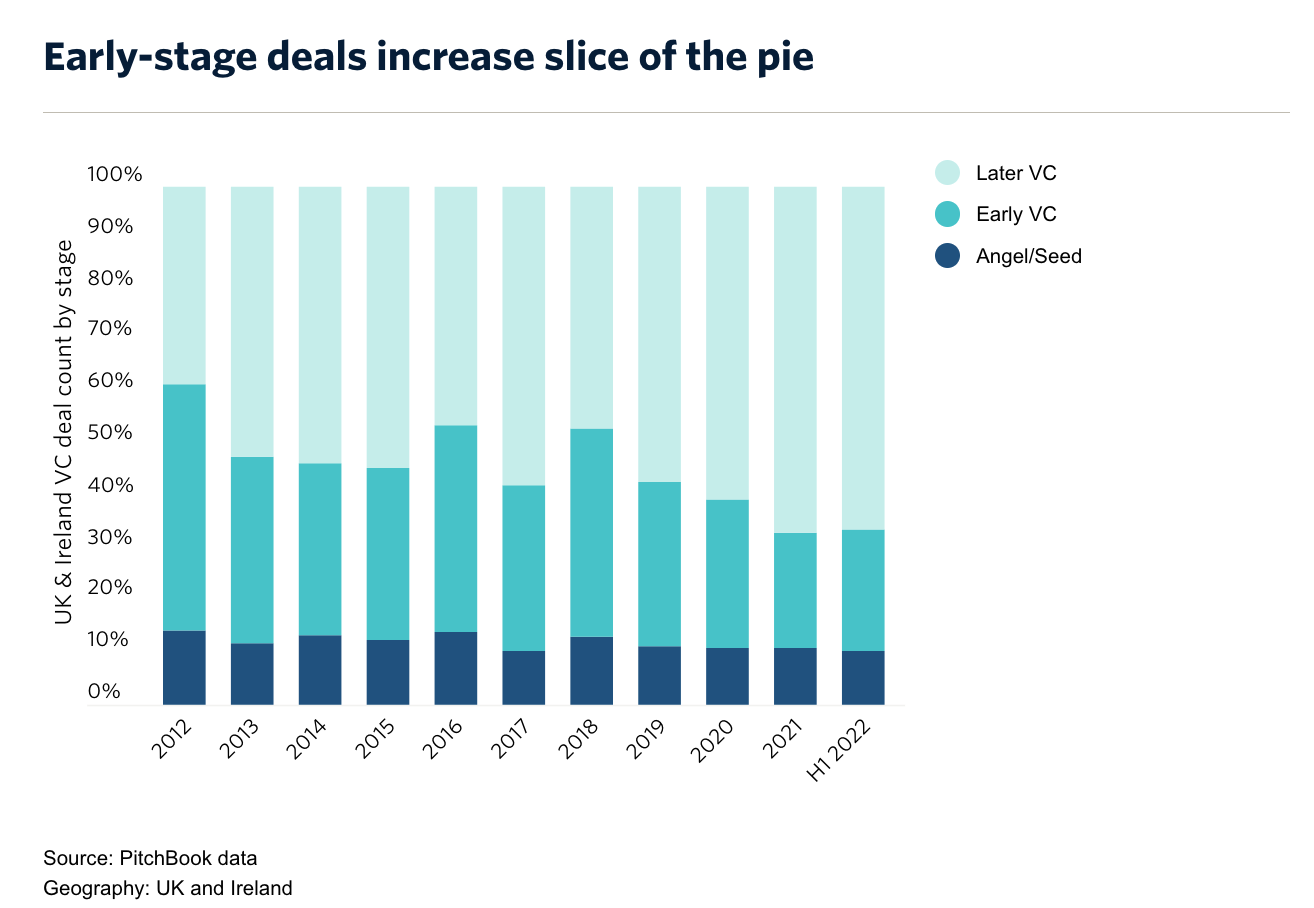

Late-stage deals accounted for the largest share of deal value in the first six months of the year despite clocking in slightly less than last year’s total. The percentage of capital raised in early-stage rounds rose from 22.3% in 2021 to 23.4% of the region’s overall total in H1.

Late-stage companies are likely to suffer the most from the fallout of the downturn and if market conditions persist, investors could shift their their focus to early stage VC rounds.

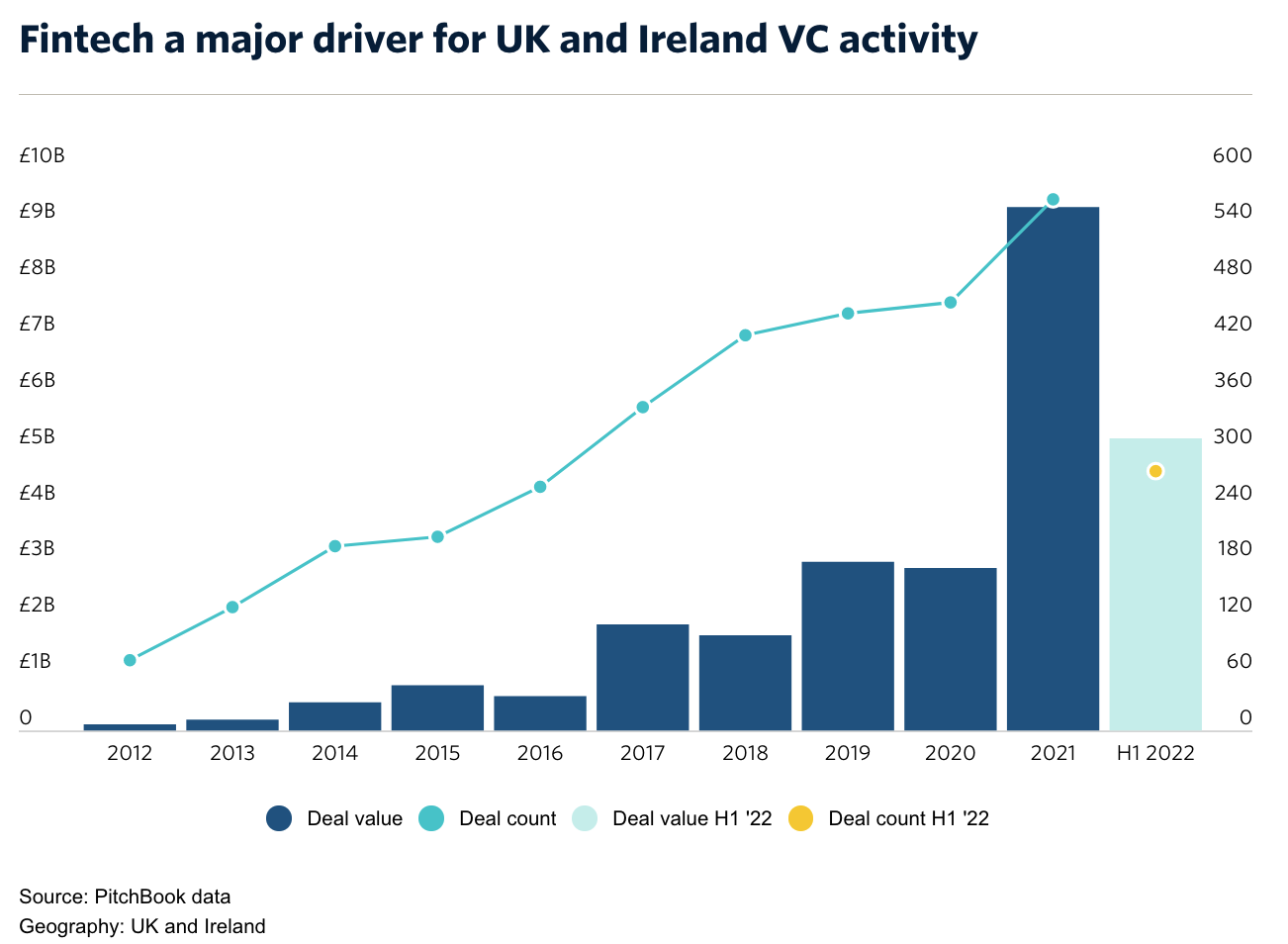

With financial services contributing £164.2 billion to the UK economy, fintech continues to drive VC activity. Deal activity in the sector has remained stable in H1 with £5.2 billion raised across 276 deals, with most of the activity in the UK.

Some of the region’s biggest VC deals this year were in fintech. The largest round was for Checkout.com‘s $1 billion Series D in January, while payment company SumUp raised €590 million (about $584.3 million) in June.

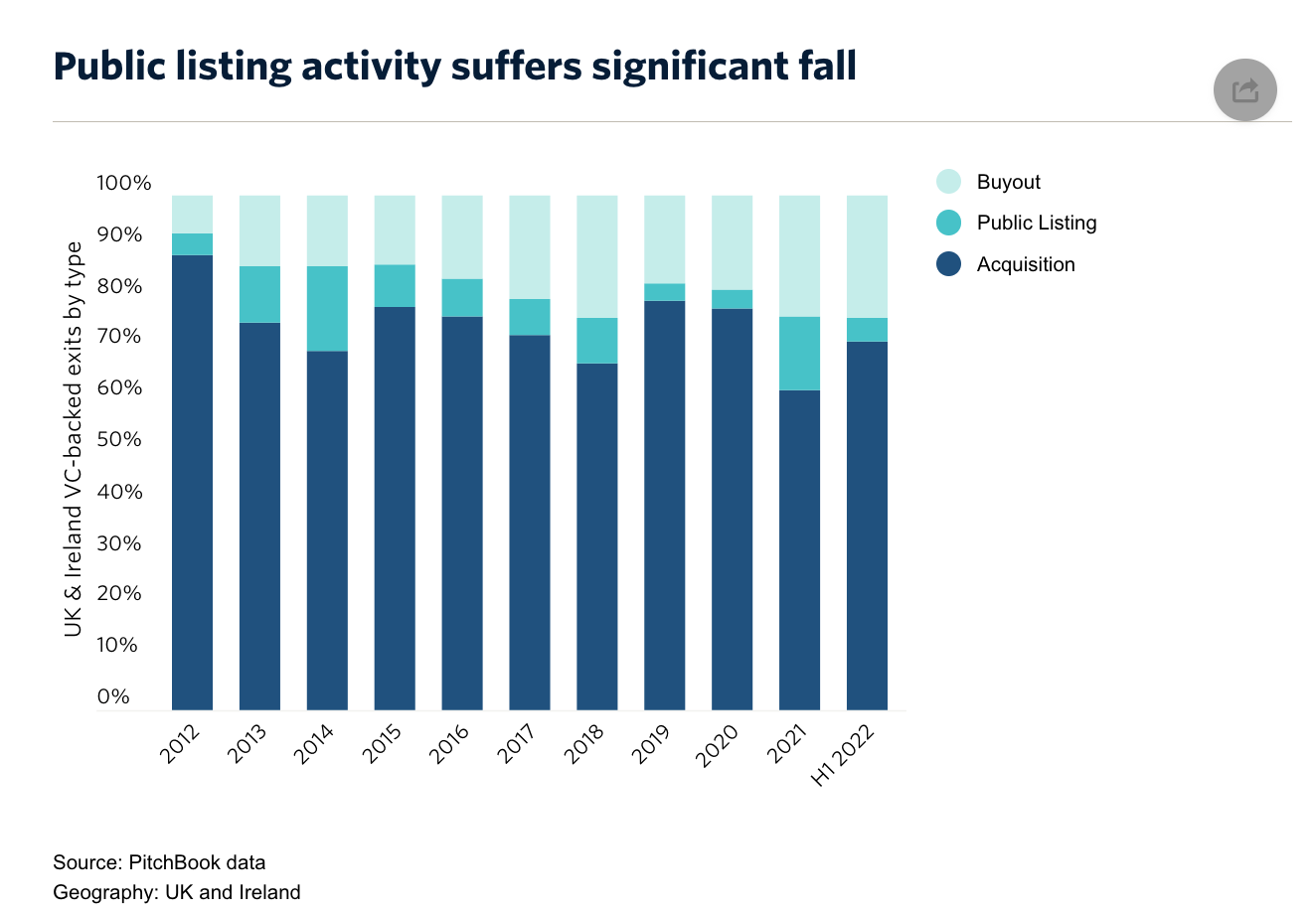

Overall exit activity returned to pre-2021 levels in H1 with public listings seeing the biggest drop. Only six such deals took place, compared to 44 in 2021.

With IPOs and direct listings becoming less appealing exit routes, acquisitions and buyouts are expected to pick up the slack. With lower valuations likely through the coming months, PE firms and corporates may have greater opportunities to pick up VC assets for less.

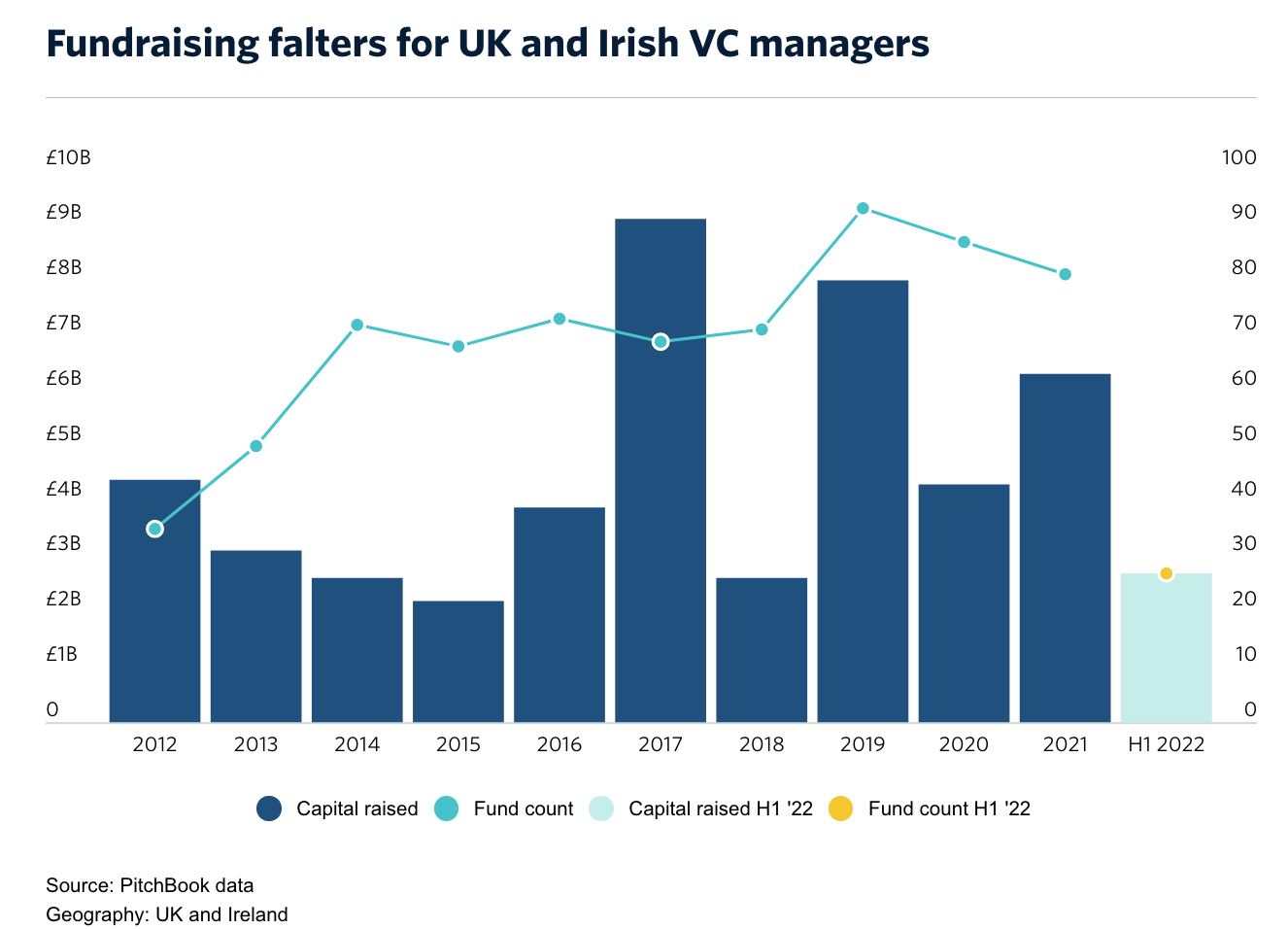

Fundraising activity has fallen behind last year’s figures, both in terms of capital raised and fund count. In H1, 27 VC funds closed with a total value of £2.7 billion.

Nevertheless, the UK and Ireland saw a handful of large fund closes in the first six months of the year. Felix Capital‘s fourth flagship fund came in at £478.5 million, followed by Blossom Capital III closing on £347.9 million.

Featured image by VectorMine/Shutterstock